bank owned life insurance regulations

The guidance attached to this bulletin continues to apply to federal savings associations. Bank Owned Life Insurance BOLI is a tax efficient method that offsets employee benefit costs.

32 Black Owned Banks And Credit Unions Sorted By State

Universal life and traditional.

. Bank-owned life insurance BOLI is a form of life insurance used in the banking industry. Bank-Owned Life Insurance Life insurance is regulated primarily by the states. Bank Owned Life Insurance and Tax Reform.

Banks can purchase BOLI policies in connection with employee compensation and benefit plans key person insurance insurance to recover the cost of providing pre- and postretirement employee benefits insurance on borrowers and. Banking organization insurance programs include the funding of employee benefits through purchases of corporate- or bank-owned life insurance and the transfer of insurable risks through coverages associated with risk management initiatives. Financial institutions supervised by the Federal Reserve also engage in functionally regulated insurance.

The OCC has indicated that the gains from BOLI cannot exceed the costs they are intended to offset. National banks may purchase and hold certain types of life insurance under 12 USC 24 Seventh which provides that national banks may exercise all such incidental powers as shall be necessary to carry on the business of banking. Done properly BOLI may offset the current and future costs of pre- and post-retirement medical coverage group life retirement.

It is a Single Premium Life SPL general account participating whole life insurance contract that is a MEC at issue. The bank pays Types of BOLI products General Account BOLI Separate Account BOLI Hybrid BOLI. The bank pays the premium owns the cash value of the policies and is the beneficiary of the insurance.

Bank Owned Life Insurance Rules and Regulations The Interagency Statement on the Purchase and Risk Management of Life Insurance OCC 2004-56 provides general guidance for banks and savings associations regarding supervisory expectations for the purchase and risk management for Bank Owned Life Insurance BOLI. Each year that the bank has the policy in place it must file Form 8925 Report of Employer-Owned Life Insurance Contracts with the IRS. Each year there is an increasing amount of Bank Owned Life Insurance BOLI purchased in the United States.

A financial institution purchases life insurance on a select group of key employees. Most BOLI programs regardless of contract type selected are designed with a single premium. Banks use it as a tax shelter and to fund employee benefits.

The interagency statement also provides guidance for split-dollar arrangements and the use of life insurance as security for loans. It should be noted that BOLIs current tax benefits have been unsuccessfully challenged over the years. The bank purchases and owns an insurance policy on an executives life and is the beneficiary.

The contract includes an Amendment to Dividends and Cash Surrender Provisions. A life insurance policy you can buy to insure the lives of your key employees. But if they are not grandfathered they may be surrendered for their cash surrender values.

Written consent is obtained from all individuals to be insured. The Office of the Comptroller of the Currency the Board of Governors of the Federal Reserve System the Federal Deposit Insurance Corporation and the Office of Thrift Supervision have issued the attached interagency statement on bank-owned life insurance BOLI to remind. What other limitations exist to the purchase of Bank Owned Life Insurance BOLI.

Under most state laws there are two regulatory regimes for permanent including BOLI contracts. This tax-advantaged asset acts similarly to a bond allowing banks to offset the expenses needed for superior benefits andor informally fund executive benefits. One based on benefits and one based on capital.

As the policys owner and beneficiary your bank harnesses unique benefits. There are two basic tests. The OCC has been the lead regulator in this area.

BOLI or bank-owned life insurance is just what it sounds like. 5 When the employee leaves the company whether through termination or retirement the bank keeps the policy in place to continue covering the benefits of other employees. How BOLI works The bank purchases life insurance on the lives of a group of employees such as executives and officers that participate in the banks benefit plans.

Cash surrender values grow tax-deferred providing the bank with monthly bookable income. The federal banking agencies are issuing the attached Interagency Statement on the Purchase and Risk Management of Life Insurance to institutions to help ensure that their. Listed below are the primary reasons why two-thirds of the banks own BOLI.

Life insurance may not be purchased to generate funds for the banks normal operating expenses except in connection with employee compensation and benefit plans for speculation or for the primary purpose of providing estate-planning benefits for bank insiders unless it is a part of a reasonable compensation package. According to the FDIC in 2021 66 of all US banks owned BOLI. Mutual Life Insurance Companys Northwestern Mutual Bank Owned Life Insurance BOLI product.

If the tax treatment of Bank Owned Life Insurance BOLI changes existing plans may be grandfathered. Written consent is obtained from all individuals to be insured. HOW DOES IT WORK.

The financial institution is the premium payer the owner and the beneficiary of the life insurance policies. Bank Owned Life Insurance BOLI Bank Owned Life Insurance BOLI is defined as a company owned insurance policy on one or more of its key employees that will informally fund the financing of employee benefits programs. BOLI is life insurance owned by the bank and issued on the lives of bank employees and directors.

The bank purchases life insurance on the lives of a group of employees such as executives and officers that participate in the banks benefit plans. National banks may purchase and hold certain types of life insurance called bank-owned life insurance BOLI under 12 USC 24 Seventh. The insured employees have no.

Bank owned life insurance is a low-maintenance asset that involves. Purchase and Risk Management of Life Insurance to institutions to help ensure that their risk management processes for bank-owned life insurance BOLI are consistent with safe and sound banking practices. Of the many tax law changes enacted as part of the Tax Cuts and Jobs Act of 2017 TCJA one provision is raising concern among banks involved in certain post-2017 acquisitions of target banks with ownership in bank-owned life insurance BOLI policies.

The federal banking agencies are providing guidance on the safe and sound banking practices they expect institutions to employ for the purchase and ongoing risk management of bank-owned life insurance. A significant concern for banks is the credit.

What Is Life Insurance An Honest Guide Updated 2022 Policyadvisor

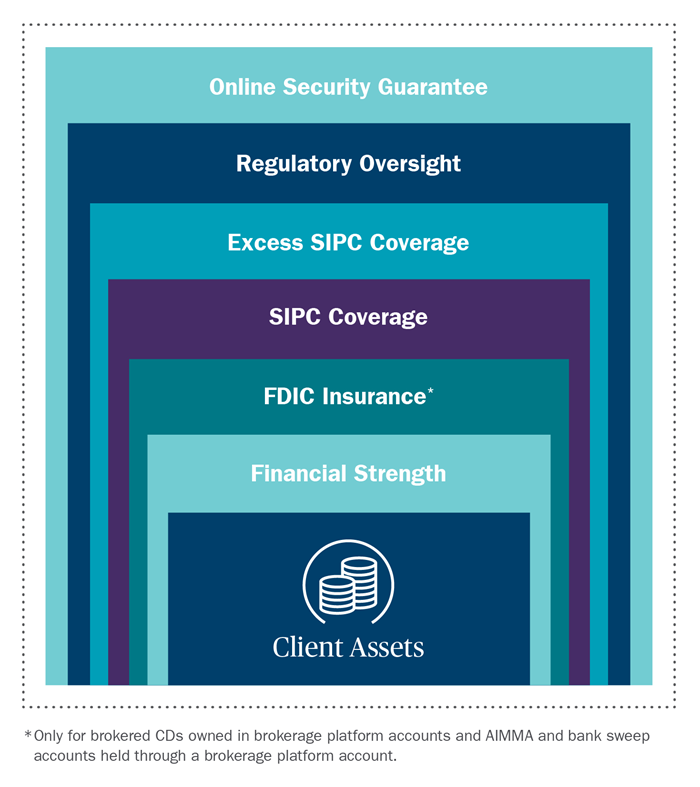

Understanding Sipc And Fdic Coverage Ameriprise Financial

Private Family Banking System With Whole Life Insurance Paradigm Life

Why Are Businesses Purchasing Life Insurance On Their Employees West Sound Workforce

2

Bank Loan For Export Business Visual Ly Export Business Bank Loan Business

Common Mistakes In Life Insurance Arrangements

Brief History Of The Company Bni

Bank Owned Life Insurance Boli

Hsbc Insurance Intends To Buy Pnb Stake In Canara Hsbc Obc Life Insurance Businesstoday

Pin On 2021

/hsbc-branch-in-new-bond-street--london-533780165-ff99ebc393c243cba463ea80559836b0.jpg)

Bank Owned Life Insurance Boli

/dotdash-insurance-companies-vs-banks-separate-and-not-equal-Final-9323c943f9974aad96b2c70d6e3aa577.jpg)

Yibxsz82aozpim

Climate Change Bank Negara Malaysia

Understanding Life Insurance Policy Ownership The American College Of Trust And Estate Counsel

/GettyImages-1065978584-59f818c896ed4f83b756fccc0e540c31.jpg)

Company Owned Life Insurance Coli Definition

How Does Life Insurance Work Forbes Advisor

Brief History Of The Company Bni

Bank Safety And Soundness Regulatory Service Lexisnexis Store